Although Stocks for the Long Run has gone through multiple iterations since it was first published in 1994, the overall theme remains the same: No other liquid asset class can compare to the performance of equities.

The author, Wharton Business School professor and MIT graduate Jeremy Siegel, concludes a diversified portfolio of equities provides the best method for most investors to build long-term wealth.

At face value, this statement may seem simple and straightforward. However, as Siegel outlines in his book, stocks have not always been the asset class of choice.

For most of the 19th and early 20th centuries, bonds and gold were the investment of choice for retail investors. Even today, financial experts debate how much of a portfolio should be comprised of stocks versus bonds.

In his book, Siegel provides decades of interesting research based on market history and analysis in Stocks for the Long Run to conclude that stocks are the best wealth-creating asset class for investors.

Who would benefit by reading Stocks for the Long Run?

Any individual investor, finance professional, or market enthusiast wanting to better understand the stock market history and performance can benefit from Siegel’s research. Even if you’ve been investing awhile, Stocks for the Long Run provides valuable historical references to support Siegel’s theory.

Learning the details of important historical market events can help you spot cycles and make better investment decisions. Siegel details most of the important market events that have occurred since the 1800s. In updated versions of his book, he provides insightful commentary on the 2008 Financial Crisis. As you read the book, you will better understand market history to apply in the future.

If you’re a nervous equity investor, this book can provide information to ease your concerns.

For new and experienced investors alike, the thought of having a 100% equity portfolio may seem especially risky. Markets seem irrationally volatile and the risk of loss may appear immense.

However, Siegel’s analysis and historical support will ease the minds of new investors. You’ll have the needed confidence to invest in equities after reading his book.

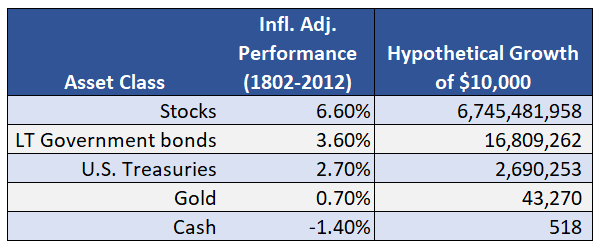

Asset returns since 1802

Throughout Stocks for the Long Run, Siegel provides his in-depth research that led him to conclude stocks represent the best asset class for most investors.

Siegel analyzes the “real total returns” (i.e. after adjusting for inflation) of the following asset classes:

- Stocks

- Long-term government bonds

- U.S. Treasury bills

- Gold

- U.S. Currency (i.e. cold, hard CASH)

Even considering the Civil War, Great Depression, Great Recession, and other market events, Siegel explains how stocks outperform all other asset classes over extended periods of time.

Especially when adjusting for inflation, bonds, gold and cash cannot compete with the returns of equities and dividends – especially when the interest and dividends are reinvested into the same asset class.

Stocks have outperformed long-term bonds by 3% per year since the early 1800s. U.S. Treasury bills have only outpaced inflation by 2.7%, and gold has barely kept pace with inflation. Clearly, a portfolio of cash has had negative returns since 1802.

Among the 5 options, stocks by far provide the best wealth-building possibilities.

Market evolution

Throughout the book, Siegel walks readers through the evolution of financial markets.

He divides U.S. market history into three subcategories:

- 1802-1870 as the U.S. transitions from an agrarian to an industrialized economy

- 1871-1925 as the U.S. gains political prominence

- 1926-present covering the Great Depression, postwar expansion, tech bubble of the early 2000s, and 2008 Financial Crisis

He explains how stocks were initially “deemed the province of speculators and insiders” and not for conservative investors in the first half of the twentieth century. Common investment thought at the time centered around bonds and gold.

However, prominent economists and analysts began researching stock performance and how equities may impact a portfolio. In 1925, Edgar Lawrence Smith published his research findings that began shifting the portfolio theory of the time. Stocks no longer became taboo. Instead, they became an investable asset class.

However, the stock crash of 1929 caused an entire generation to again shun stocks. Siegel explains that although the market crash and ensuing Great Depression wreaked havoc on American society, the decline is only a small “blip” on the chart of total stock market returns. In fact, $1 invested in 1802 would be worth nearly $14 million today despite the Great Depression, Tech Bubble, and Great Recession.

If you’re interested in the historical perspectives of investing, Siegel chronicles market performance of stocks, bonds, gold, and cash while outlining market and political events from the 1900s through The Great Financial Crisis of 2008 that impacted their returns.

Increasing Shareholder Value

If you’re worried that Stocks for the Long Run is just a boring history book, then have no fear.

While Siegel provides plenty of historical context on market behavior, the evolution of financial products (such as the index fund), tax policy evolution, and political events that impacted the market, his book is far from just a market history book.

For those interested in learning about what makes stocks inherently valuable, Siegel provides the answer.

He explains that the fundamental source of asset values are derived from the expected future cash flows that companies generate. For stocks, Siegel contends earnings (or the potential for future earnings) and dividends (or potential for future dividends) drive the value of equities.

Then, these future cash flows are brought to present value using a particular discount rate.

Discounting is necessary because of 3 primary reasons:

- Risk-free rate: investors have the opportunity to earn a guaranteed return by investing in government-backed treasuries

- Inflation: erodes the value of future cash flows

- Risk premium: future cash flows vary in magnitude of risk depending on the particular company. Therefore, investors require a premium to compensate them for these securities

Sources of Shareholder Value

Siegel explains that earnings are the main source of value for shareholders. Earnings are the source of cash flow to shareholders.

Retained earnings create value 4 primary ways:

- Debt reduction

- Business investment (capital projects that produce incremental cash flow)

- Investment in equities, assets, or acquisitions

- Share repurchases (buybacks)

If you’re interested in more technical finance concepts, Siegel provides enough finance to scratch this itch.

Siegel discusses stock valuation using various methods including the Gordon Dividend Growth Model and using “yardsticks” for comparative company analysis.

The most popular “yardstick” that Siegel explains is the use of the Price/Earnings Ratio. This ratio compares the market value of a company to the earnings it produces. Then, an investor can compare to other companies (or the overall stock market) to quickly gauge whether the security is undervalued.

Outperforming the Market

If you’re looking to read about the stock market and investing, chances are your primary, underlying goal is to beat the market.

While investing passively in index funds will certainly build wealth over time, identifying methods to provide incremental returns can help supercharge your savings goals.

In Stocks for the Long Run, Siegel provides analysis to help readers identify stocks that outperform the market.

According to Seigel, investors tend to be drawn to firms that generate high earnings and revenue growth. However, empirical date shows investing in these companies tends to lead to subpar returns.

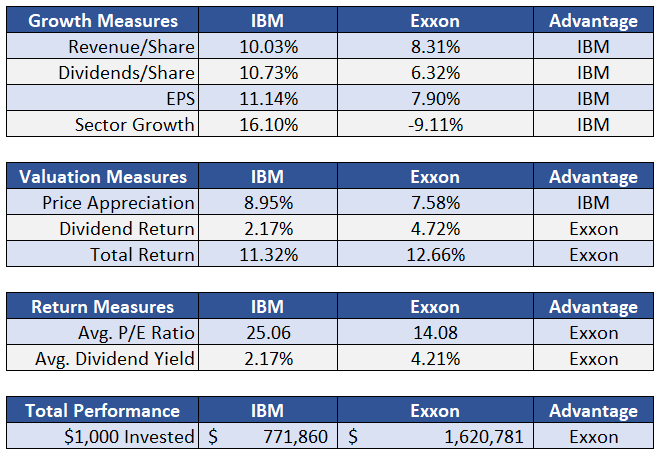

Exxon Mobil vs. IBM

To demonstrate his point, Siegel compares a $10,000 initial investment in the mature, oil and gas stalwart of Exxon Mobil to IBM from 1950-2012.

In 1950, IBM was a small, promising technology company that would one day morph into a behemoth Fortune 500 company. Over the next 6 decades, IBM would beat Exxon in nearly every category of growth as shown below.

However, even though the oil and gas sector as a whole declined nearly 10% while the technology sector grew over 16%, Exxon outperformed one of the most prominent technology companies of the 20th century.

How was this possible?

Siegel contends the primary reason Exxon beat IBM was because of VALUATION.

Even though IBM grew revenue and earnings (and share appreciation) at faster rates, shareholders valued IBM nearly 2x higher compared to Exxon.

Further, the compounding of dividends over the decades contributed to the overall returns. Because Exxon was valued less in the market, its dividend yield was substantially higher, allowing investors in Exxon to accumulate 12.7x the number of shares they started with. By contrast, IBM investors would only accumulate 3.3x their original shares.

For this reason, Siegel contends that valuation and dividends play a key role in identifying stocks that will outperform.

Smaller Capitalization Stocks Generally Outperform

As most investors would expect, smaller companies tend to outperform larger capitalization stocks over the long-term.

However, small and mid-cap companies experience much more volatility. Often, small and mid-cap earnings and growth are much less predictable as these companies mold themselves into the next global powerhouse.

For this reason, the magnitude of small-cap stock outperformance has varied over the past 86 years.

Total nominal returns for the S&P 500 have averaged 9.69% per year since 1926. By contrast, small-cap stocks have averaged 11.52%. However, much of the outperformance of small-cap stocks stems from an explosion in small-cap stocks between 1975 and 1983. During this period, pension and institutional managers were drawn to these smaller, growth-oriented companies after the collapse of large-growth stocks.

When this period is excluded in Siegel’s analysis, small-cap stocks performed in line with the S&P 500.

Therefore, Siegel would content that investors who implement a portfolio comprised of smaller capitalizations stocks across a variety of industries would diversify against much of the market risk. Often, when combined with dividend-paying, value stocks, these portfolios reap the greatest returns and outperform the overall market.

Stocks Tend to Revert to the Mean

When investors enjoy periods of market exuberance, the market tends to find balance by reverting to the mean. This behavior results in short-term volatility.

However, in the long run, the market tends to increase nominally between 8-10% annualized. For the investor who chooses to buy and hold stocks, their portfolio may be volatile. However, in the long run, investors should profit by taking on the risk of equity ownership.

Stock returns are often tied to the overall business cycle

Almost without exception, the stock market turns down prior to recessions and rises prior to economic recoveries.

In fact, 90% of recessions have been preceded by declines of 8%+ in the market. Therefore, the market is closely related to the economic cycle.

If investors could learn to predict in advance when recessions will begin and end, they could enjoy superior returns. However, it’s virtually impossible (even for renowned economists) to predict the business cycle.

Therefore, Siegel concludes that the worst strategy investors can take is to follow the prevailing sentiment about market activity. This would lead investors to “buy high and sell low.” Currently, forecasters have not yet identified a precise way to predict economic activity. For this reason, a buy and hold strategy will be best for most investors.

Structuring a portfolio for outperformance

In the latter part of Stocks for the Long Run, Siegel summarizes his theory on how to be a successful investor.

To get the details, consider purchasing the book.

However, here are the 6 keys Siegel presents for successful investing:

1. Keep expectations realistic

Historically, stocks have returned 6%-7% after inflation. Over the course of history, markets have sold at an average P/E ratio of ~15.

When P/E ratios are higher (like today), investors should assume lower future returns. The opposite is true when P/E ratios are lower.

2. Invest for the long-term

Stocks are a fairly stable asset class over longer durations. However, in the short-term, stocks can be very volatile.

Your portfolio allocation depends on personal circumstances and your own risk-tolerance. In Chapter 6, Siegel proves how over holding periods of 20+ years, stocks have both higher returns and lower after-inflation risk than bonds.

As your investment horizon becomes longer, consider putting a larger percentage of your investable assets in equities.

3. Invest most of your stock portfolio index funds

One of his chapters is devoted to showing how broad-based indexes have outperformed 2 out of 3 mutual funds since 1971.

Further, investors should look for low-cost funds with annual expense ratios below .15%.

A portfolio of equal-weighted or value-oriented index funds can help you outperform the market.

4. Invest at least 1/3 of your portfolio in international stocks

Today, the U.S. contains only 50% of the world’ capital. Further, foreign companies are gaining rapidly as other countries develop.

Therefore, including growing economies is an important part of portfolio allocation. However, Siegel warns not to overweight high-growth countries whose markets exceed 20x earnings.

5. Look for “value stocks”

Essentially, the whole thesis around Stocks for the Long Run contends that value-oriented equity stocks will outperform all other asset classes.

Stocks with low P/E ratios and higher dividend yields have superior returns and lower risk that growth stocks. Therefore, Siegel recommends tilting your portfolio towards value by buying indexed portfolios composed of value stocks.

6. Maintain disclipline

Perhaps, maintaining disciplined approach is the hardest rule to implement.

As humans, we’re all emotional – especially, when it comes to our hard-earned money. The theory of Loss Aversion states that as humans, we would rather avoid a loss rather than acquiring equivalent gains. For instance, it’s better to NOT lose $5 rather than finding $5 on the ground.

Often, this makes us risk-averse. When markets begin to plummet, we’re tempted to cut our losses and run for the hills.

However, we must resist selling when the market declines and buying when investors are bullish. In Chapter 22, Siegel explores the concepts of behavioral economics to help you avoid the psychological investors.

Buy and Hold Stocks for the Long Run by Jeremy Siegel

In Stocks for the Long Run, Siegel outlines and defends the thesis for investing in stocks over the long-term.

He offers facts and figures that back up his assumptions. He showcases stocks that do tend to outperform other asset classes over longer durations. While bonds outperform stocks around 40% of the time for periods less than 5-years, over a 30+ year time horizon, no asset class has outperformed a well-diversified portfolio of equities.