Founded in 2008 and with over $16.4 billion in assets under management as of April 2019, Betterment provides an online robo-advisor platform that invests in a portfolio of low-cost, exchange-traded funds (ETFs).

By answering a series of questions regarding your investing purpose and tolerance for risk, Betterment automatically compiles a portfolio of low-cost ETFs to match your investing profile. As the stock market continually adjusts in price, Betterment automatically re-balances your portfolio to help you stay on track and reach your investing goals.

Who is Betterment’s Target Audience?

While no investing should ever be completely hands off and you are ultimately responsible for monitoring your portfolio’s performance, Betterment greatly reduces that amount of time needed to research and select individual ETFs.

For most Americans, a more passive approach to investing provides the best results. Rather than investing time researching ETFs for your particular goals, simply provide the information to Betterment. After answering a series of questions, the robo-adviser will do the work of selecting ETFs for you.

For individuals looking to avoid the hassle of identifying index funds fitting to your personal goals, Betterment may be worth the .25% asset management fee. In exchange, you receive their service of recommending and managing your portfolio.

While this fee is generally higher than buying the respective ETFs directly from Vanguard (where fees range from .02%-.07%), Betterment claims to increase returns for retirement savers by more than 1.48% compared to returns of the typical investor.

Therefore, Betterment offers a very user-friendly platform for new investors or for those that do not wish to spend a lot of their free time monitoring their portfolio.

Even if you do enjoy managing your own portfolio, further diversifying through an index strategy with Betterment could help alleviate any “user error” from bad investment choices.

How Will Your Be Capital Invested?

Through a variety of low-cost ETFs, Betterment automatically allocates and re-balances to optimize your portfolio. Each time you make contributions or the stock market shifts, you can be sure your portfolio will stay aligned with your pre-set strategy.

Before we explore further let’s answer this simple question for any novice investors…

What is an ETF?

An exchange-traded fund (ETF) is a publicly-traded investment that acts very much like a normal stock. However, unlike an individual stock which represents equity ownership in a particular business, an ETF is generally comprised of hundreds (or thousands) of individual stocks.

ETFs can be designed to track certain industries, benchmarks, or segments of the market. As an example, ETFs have been designed to track the overall market (S&P 500). You can find ETFs that mimic particular foreign stock markets, bond market, or even particular industries. Sector ETFs provide exposure to industries ranging from healthcare to the commodities market.

With each dollar you invest into an ETF, you achieve instant diversification as your dollars are automatically divided among all of the represented companies in the fund.

Instead of buying shares of hundreds of companies’ stock and paying $4.95-$10 per trade, indexing allows you to simply purchase one, commission-free fund. This saves you thousands of dollars in commissions.

Which ETFs does Betterment Offer?

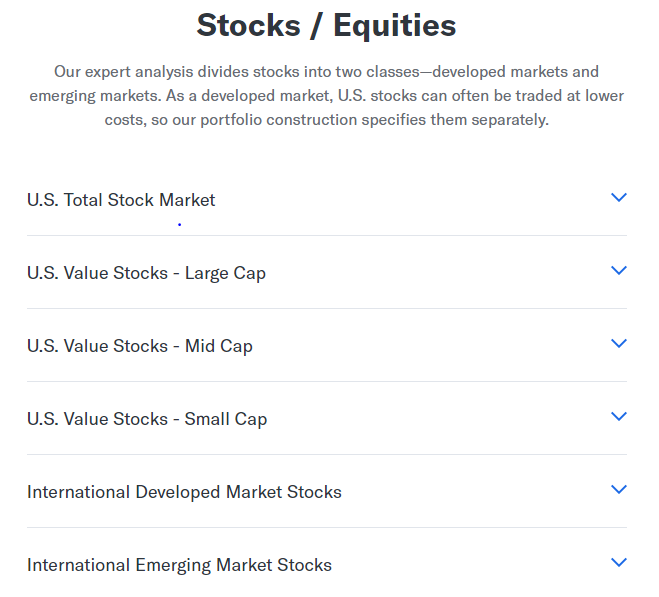

For equity investments (stocks), Betterment offers 6 categories of multiple ETFs designed to achieve certain goals.

Here are the primary equity categories:

Each of these categories is designed to track particular segments of the market.

U.S. Total Stock Market

Through the Vanguard Total Stock Market Index (VTI), investors achieve broad exposure to stocks in the U.S. Market.

Based on Betterment’s risk-management and portfolio philosophy, American companies represent a significant portion of developed market stocks and generally correlate with other markets. However, when combined with international developed market and emerging market stocks, your portfolio achieves greater diversification.

By purchasing a U.S. Total Stock Market Index, you are placing a “bet” on the overall American economy. Unlike an S&P 500 index fund (which represents the 500 largest domestic companies), the VTI fund also encompasses relatively smaller companies. This gives you exposure to smaller companies that have the potential to become the next Amazon or Apple.

U.S. Value Stocks – Large-Cap, Mid-Cap, and Small Capitalization Stocks

One of the most famous “value investors” is none other than Warren Buffet. By investing in companies with valuation metrics (price/earnings, price/book, price/sales, etc.) that are lower than other companies or below their “intrinsic value,” investors such as Buffett have beaten the overall market.

Therefore, value funds seek to focus on companies that are undervalued and have the potential to outperform their peers.

Primarily through the Vanguard Value ETF (VTV – .04%), Vanguard Mid Cap Value (VOE – .07%), and Vanguard Small-Cap Value (VBR – .07%), Betterment provides exposure to both large and small companies that the fund managers have identified as undervalued relative to their valuation criteria.

Through VTV, investors gain exposure to large companies with low valuation metrics. Examples include Berkshire Hathaway, Johnson & Johnson, and JP Morgan.

Through the VOE, you’ll gain exposure to slightly smaller companies with room to grow. These companies include Newmont Goldcorp, Motorola, and M&T Bank.

For small, relatively undervalued companies including IDEX Corp and Atmos Energy, you will gain exposure to this segment of the market through VBR.

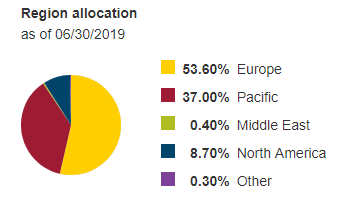

International Developed Markets

By investing in the Vanguard FTSE Developed Markets ETF (VEA – .05%), Betterment provides exposure to a broad collection of stocks from non-U.S. developed markets such as the United Kingdom, the European Union, Japan, and other developed countries.

While the stocks in the FTSE have a similar risk and return profile as the U.S. Total Stock Market, investing outside of solely the United States provides for an extra element of diversification.

Through the VEA, you’ll own some of the largest global companies in the world including Nestle SA, Royal Dutch Shell, Toyota, and Samsung.

Even though the FTSE has underperformed the S&P 500 over the last several years, gaining international exposure generally should reduce volatility and provide stability to your total portfolio.

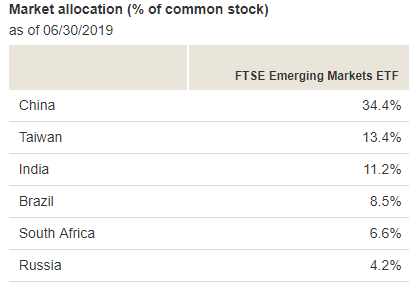

International Emerging Markets

By purchasing the Vanguard FTSE Emerging Markets ETF (VWO – .12%), investors gain exposure to a broad collection of stocks from emerging markets. These markets include China, Taiwan, India, Brazil, Russia, Thailand, and South Africa, among others.

Generally, International Emerging Market Stocks involve greater volatility and risk compared to other developed markets. However, by assuming more risk, your investment in these markets may lead to higher growth as developing states modernize and gain wealth.

Emerging market stocks also result in diversification as they are generally not correlated to U.S. and other Developed Markets.

The primary underlying companies in VWO include Tencent Holdings, Alibaba, and Taiwan Semiconductor Manufacturing Company.

By investing in International Emerging Markets, you gain access to relatively large capitalization companies that have the potential for explosive growth as they expand and their domestic markets continue developing until maturation.

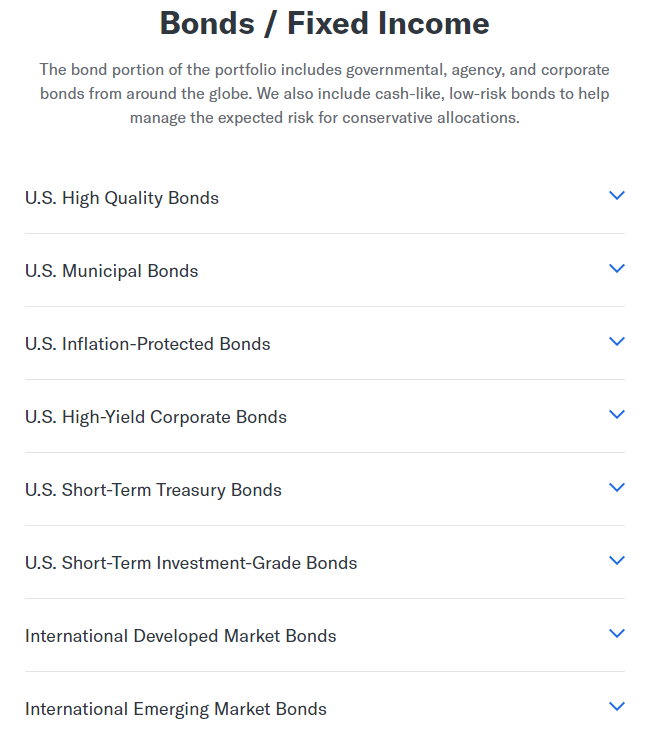

Bond/Fixed Income ETFs

For those looking for a more “guaranteed” source of income, bond funds offer investors relative stability through their contractual interest payments.

What are Bonds?

Bonds are debt instruments issued by companies or governments to fund operations, invest or expand the business, provide civic benefits, or even payoff higher-yielding debt.

Bonds are rated by “independent” rating agencies based on the issues relative risk and likelihood of default. Highly rated debt generally receives a lower interest rate since there is less overall risk of default. Conversely, over-leveraged, declining companies or governments generally receive a lower rating and a higher interest rate that corresponds to the increased risk of default.

Corporate Bonds

While companies certainly may default on their debt due to overleverage during market or industry downturns, debt holders have preference over shareholders in the event of liquidation or restructuring. For this reason, the cost of debt is generally “cheaper” than the cost of issuing new equity. This is because debt holders have some level of recourse.

For this reason, many companies (especially in stable, capital intensive industries) employ a hefty percentage of their enterprise value by issuing debt. This reduces their weighted-average cost of capital (WACC). In turn, this allows shareholders to receive a higher return on their equity ownership.

Government Bonds

When you purchase a particular bond fund (such as U.S. Municipal Bonds or Short-Term Treasury Bonds), you purchase bonds issued and backed by the full faith of the particular municipality, state, or even our own federal government.

State and municipalities do not have the power to print money like the federal government. However, they do have power to tax their constituents if necessary. Even with this ability, there are still certain risks associated with state and municipal bonds.

Because the U.S. Treasury has some power to control the money supply by printing more currency and U.S. debt is backed by the credit of the U.S. Government, Treasury Bills (T-bills) are considered “risk-free.” Since investors could theoretically buy a guaranteed return at the risk-free, T-bill interest rate, Treasuries are the basis in which we analyze or benchmark other debt instruments.

For example, if the 2-year Treasury yields 2.2%, investors would require a higher percentage return for a corporate bond due to the possibility of default. Some corporate debt issued by extremely stable, well-capitalized companies may have a yield near Treasuries. Alternatively, other riskier debt may result in a much higher spread in interest rates.

Higher yields compensate investors for their speculation or the risk that the company defaults.

How Should Bonds Be Used in Your Portfolio?

Now that we have geeked out in the world of finance for a bit, the bottom line is that debt investors are generally more willing to accept lower returns for greater stability compared to equity investors.

By investing in bond funds, you are purchasing a piece of hundreds or thousands of individual bonds. These bonds range from corporate debt to federal, state, and local government bonds.

Who Should Add Bonds to Their Portfolio?

While you must certainly assess your own financial situation and risk tolerance, bonds are typically reserved as a “wealth preservation” tool rather than “wealth creation.”

Therefore, financial planners will generally recommend that younger investors allocate either none or a very low percentage of their portfolio in bonds. Because you still have a 20, 30, or 40-year career to earn and invest money, you have a time horizon conducive to risking more of your capital in the market. In turn, you should receive substantially higher equity returns. Plus, younger individuals should be focused on growing their net worth as they have not yet achieved a portfolio capable of sustaining financial freedom or retirement.

However, as we age and reach our late 40s and 50s, adding fixed income funds will reduce volatility and continue spinning off cash flow in your portfolio. Even at 50, if you plan to continue working and earning an income well into your 60s, you may wish to maintain a strong equity position.

As the market generally experiences a 10% pullback each year and loses money overall on average once every three years, you should not invest capital in the stock market that you need in the next five years. Therefore, a portion of the capital you need in the next 5 years should be allocated to short-term investments. This includes liquid money market accounts and short-term Treasuries.

Here are the various bond funds offered by Betterment:

My Personal View on Bonds

This section is solely my own opinion on bonds and to offer a different perspective from the conventional portfolio planning community. This information does not constitute a recommendation for your personal situation.

While certain rules-of-thumb recommend equities only comprise “100 minus your age,” I do not plan on adding bonds in my own portfolio into well into my 60s. At this time, I hope to no longer be generating an active income. Contrarily, if I were to follow conventional wisdom, I would need nearly 30% of my portfolio invested in bonds which would be absurd at my age.

Because of bonds’ lackluster performance relative to stocks, a perpetually low interest rate policy instituted by the Federal Reserve, and my multi-decade investing time horizon, owning ANY bonds in my portfolio at my age makes little sense. Further, by the time I reach age 50, the likelihood of living to over 100 years old becomes increasingly likely based on the trending mortality rates, medical advances, and progression of our developed society.

If I moved half of my portfolio into bonds at age 50, there is a serious chance of not having a portfolio large enough to sustain a lengthy retirement or the lifestyle I desire.

Stability Can Be Achieved Through Stocks

Further, instead of owning bonds, risk can be mitigated through a basket of stocks that imitate the similar risk profile bonds provide. After all, bonds do not come without inherent risk.

As an example, I could allocate a substantially larger portion of my portfolio to dividend paying stocks. By buying stock in stable, dividend paying companies that have yields similar to bonds (ranging from ~2%-5%), I also can realize the equity appreciation in addition to the actual cash dividend payment.

Further, certain stocks including Master Limited Partnerships (MLPs) and Real Estate Investment Trusts (REITs) yield much higher rates than typical stocks thanks to the tax treatment they receive. While these types stocks and funds generally do not experience the explosive growth that stocks such as Amazon and Facebook provide, they are generally more stable and can pay out most of their income to unit-holders. This results in yields ranging from ~3%-8%.

The bottom line is there are ways to achieve relatively more stability without giving up the equity appreciation of stock ownership.

Social Security Already Provides Annuity Payments

While many question the solvency of the Social Security Administration (SSA), I do know each month a hefty amount is withheld from my paycheck with the promise of a future return.

Whether or not the SSA is in its current form in 40 years or a new bureaucracy has taken its place, there will more than likely be some form of social entitlement program like Social Security for future retirees.

For those in retirement today, Social Security acts as a guaranteed, variable annuity that increases each year with inflation. The average monthly Social Security benefit for someone who elects to receive their payment at full retirement age is $2,861. Over the course of the year, the average retiree receives benefits of over $34,000.

In a way, Social Security acts as a $600,000 – $700,000 bond investment that yields 4%-5%. While Social Security by itself probably will not sustain a retiree’s desired lifestyle, these payments go a long way to provide stable, recurring, and “guaranteed” payments to cover basic expenses.

Because of the guaranteed payments, I can allocate a greater percentage of my portfolio to wealth-building assets like stocks and real estate.

Allow Betterment to Build Your Portfolio Based on Your Risk Profile and Goals

Perhaps, you feel a little conflicted on your portfolio allocation. The good news is that you can simply answer the questions on your goals and risk profile and Betterment will automatically account and recommend a portfolio optimized for your needs and risk tolerance.

Even after you have answered the questions posed by the robo-adviser and receive the recommended portfolio, you can customize the holdings to achieve your desired asset allocation.

Is Betterment Worth the Management Fees?

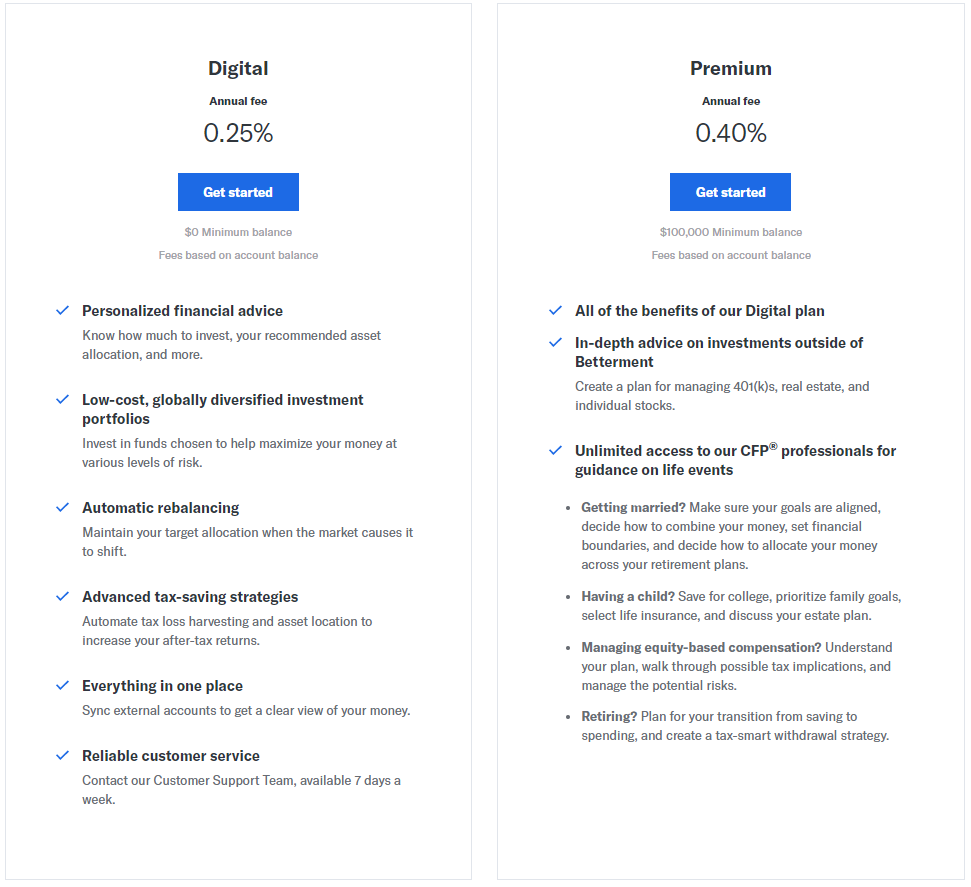

Currently, Betterment offers two portfolio plans with differing levels of service and asset requirements to help you get started.

Digital Service Plan

Through the Digital service plan, investors pay a .25% annual fee on assets under management (AUM) by Betterment. A portion if this goes to the fund manager (i.e. Vanguard). The remaining portion pays for Betterment’s service and technology.

Since there are no minimums for this plan, most investors would probably use this plan as the Premium Plan requires a $100,000 minimum balance.

As discussed, the funds Betterment implements would cost you between .03%-.07% if bought directly from Vanguard. The remaining portion of the fee stems from the services that Betterment provides which ranges from the personalized financial advice, automatic re-balancing and tax strategies, and customer service.

Ultimately, you will need to decide if the services are worth ~.2% of your invested capital.

Premium Plan

For those with $100,000 or more to invest with Betterment, you have access to the next level of services.

For .40% annually, you receive all of the previously discussed services as well as access to financial advice on other portfolios you may have. Betterment’s network of advisers can help you take a holistic approach to your entire portfolio held with Betterment as well as your 401(k), individual stocks, or even real estate.

Further the fees also include access to Certified Financial Planners (CFP) to help you navigate life events. While you certainly pay for this level of service in the .40% management fee, if you plan to utilize services from a CFP or have a more complex financial portfolio, gaining expert advice under one roof can more than pay for the cost.

What’s the Bottom Line on Betterment?

Generally, investors should strive to minimize fees as much as possible since larger than necessary fees can greatly hinder your overall returns over decades. Since most financial experts recommend keeping your all in fees below 1%, both of Betterment’s options are well below this threshold. This allows you to keep more of your money while also receiving a valuable service.

For investors that are willing to create an account with Vanguard or another low-cost index fund provider, you will probably save anywhere from .18%-.22% in fees, annually. Depending upon your invested capital, this could correlate to hundreds or even thousands of dollars in unnecessary fees if you were willing to research, monitor, and manage your own portfolio.

However, if your lack knowledge or if fear is keeping you from getting started in the first place and Betterment provides you with confidence that your portfolio is being managed well, there is no question that paying the fees would be better than not investing at all.

My Personal Views on Betterment

Personally, I love to do market research and monitor my portfolio myself. I already have multiple accounts where I implement an index fund strategy to compliment my individual stock picks. On all of my index funds, I pay expense ratios well below .25% by investing directly with my brokers. This saves me hundreds of dollars each year.

That being said, if I wanted to stick solely to my day job and had no interest in monitoring my individual portfolio, I would definitely consider investing a portion of my portfolio with Betterment.

If you do not know where to start or want a one-stop shop for a personalized indexing strategy, Betterment offers invaluable tools and resources to help you best reach your financial goals.